Down Rounds: What Every Director Should Know

A down round is a difficult economic reality for directors of a company. The name feels negative and implies a downward projection for the company. It can also have a serious negative impact on the employees, founders and early investors in the company. However, a down round is still a capital raise, and the eventual alternative to raising capital for a company that needs funding is its demise by liquidation or otherwise. Completing a down round, at least, allows the company to carry on.

So how should a board of directors, faced with a difficult funding environment, approach a down round? We cover the essentials underlying a down round, with some recommendations for boards navigating its tricky waters. This article covers:

What is a down round?

Is the company at fault?

What are the investment terms?

How does a down round impact the company’s founders and employees?

How does a down round impact the company’s investors?

How should the board authorise a down round?

Recommendations for the board.

1. What is a down round?

A down round occurs when a company issues new shares to raise capital (let’s call this the “Current Round”) at a pre-money valuation that is less than the post-money valuation of its immediately prior equity capital raise (the “Reference Round”). (“Pre-money” versus “post-money” means the valuation of the company before or after the relevant investment). Normally, a company would have an “up” round, where its pre-money valuation in the Current Round is more than its post-money valuation of the Reference Round, or at least have a “flat” round when those two valuations are the same.

By having a down round, investors that put money in the Reference Round will have their shares valued at less than their investment. Other existing investors (including founders and employees) will also end up with less economic share of the company than before the down round. A down round still means investors are putting capital into the business, albeit on a less favourable valuation to existing investors.

2. Is the company at fault?

No, down rounds can occur for several reasons. The economic conditions and market sentiment may not favour an up or a flat round. The industry in which the company is operating may be experiencing a bear market with a loss of investor interest. There could also be strategic considerations at play, such as an opportunity to bring in a key partner or investor who insists on a lower valuation than the Reference Round. Of course, underperformance can be a reason too. The company may have failed to meet its key performance indicators (such as revenue or other growth targets) agreed with investors in the Reference Round. All these factors affect whether a company carries out a down round or not.

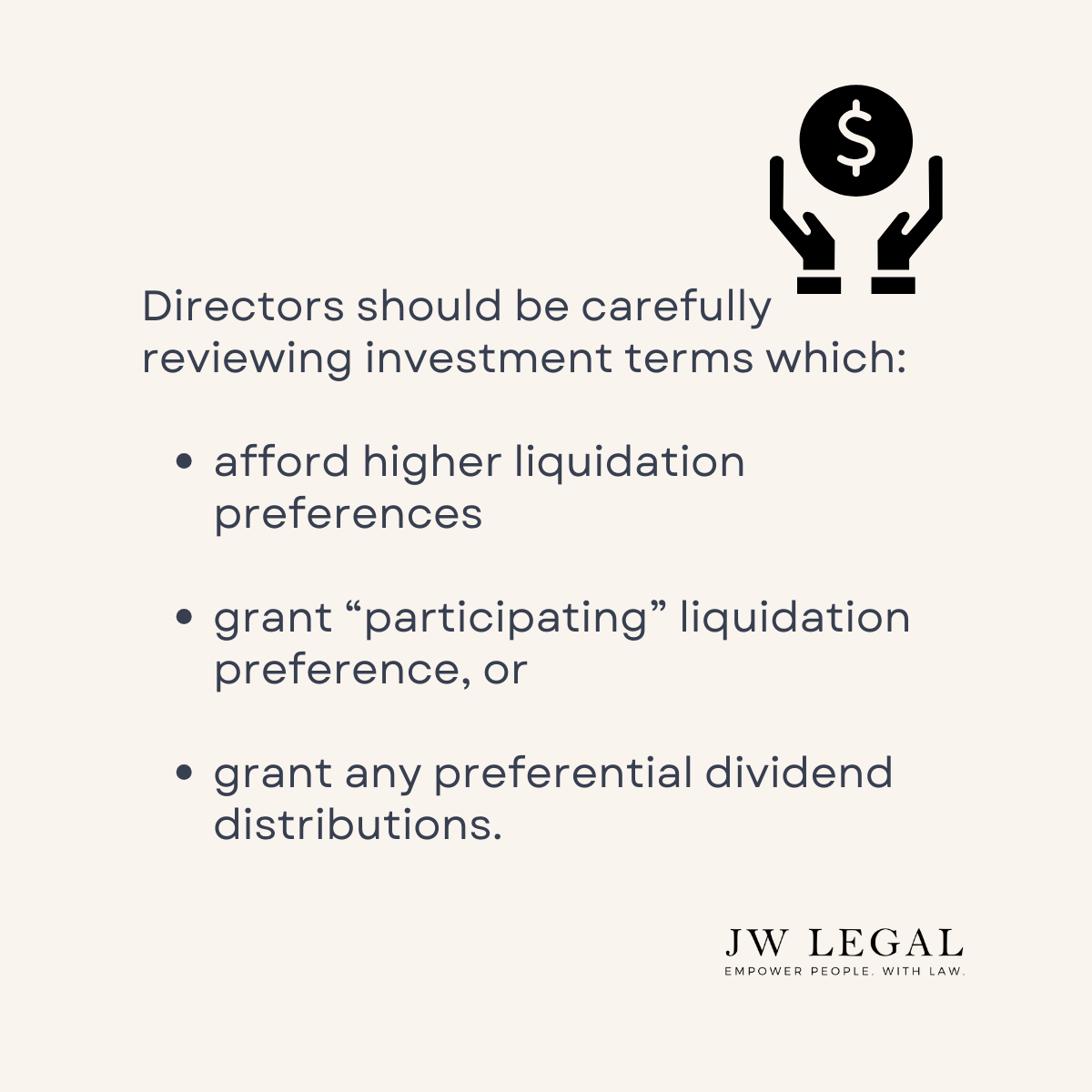

3. What are down rounds’ investment terms?

The shareholders would expect the company and the investors to negotiate key investment terms around economics and control features. Other than its valuation, do you offer board appointment rights? Approval rights over key company decisions? Preference share rights? Milestone conditions and tranched investments? These are terms you would typically negotiate with investors.

Another way to understand a down round is that the company raising capital is at its weakest point, evident in its acceptance of a lower than ideal valuation. Some investors may see this as an opportunity to take advantage of the investment terms, some of which are set out below. If you see such terms being offered or required by the investors, it is a potential sign of things to come in the company-investor relationship in the future. They are also unusual in New Zealand market. These terms include:

Higher liquidation preference – In a liquidity event (e.g. business sale), an investor with a liquidation preference can elect to demand the return on their investment or convert their preference shares into ordinary shares on a 1:1 basis to participate in the exit as ordinary shareholders. If a shareholder elects to receive their liquidation preference, this amount would be first deducted from the proceeds of an exit event, before the remaining amount (if any) is distributed to the ordinary shareholders. The election is an economic one, whichever option gives them a higher return on investment. Normally, the liquidation preference is 1 times the original investment.

While unusual, in down rounds, higher liquidation preferences may be sought. These are toxic and can have the effect of wiping out the equity value of early investors including the founders in liquidity events. The company and even new investors should have a good rationale for agreeing to liquidation preferences above a single multiple.

Participating versus non-participating – The preference shares are typically “non-participating”. This means that if a preference shareholder elects to receive their liquidation preference in an exit event, they cannot also convert their shares into ordinary shares and participate in the distribution of the remaining proceeds. Where the shares are “participating”, the preference shareholders get both the liquidation preference paid out first and then participate as ordinary shareholders in the remaining proceeds. Issuing shares with participating liquidation preference can have a depressing impact on the existing shareholders’ value.

Dividend rights – Preferred dividend rights are not unusual, but their specific terms need to be carefully negotiated. A generally acceptable preferential right would allow the preference shareholder to receive more dividends if and when a dividend is declared and paid. A more punitive, less desirable dividend right involves a fixed annual dividend right. If the company is unable to satisfy the solvency test when declaring cash dividends, the company may be required to payment-in-kind in further shares. Features such as fixed dividends including in shares is another feature that dilutes the existing shareholders’ value in the company. (And arguably designed to require the company to realise an exit event in the near future).

There are other features specific to a down round, but they stem mainly from the weakened negotiating position of the company. The drivers for asking these terms may be a tactic to obtain control over the company completeness or under an exaggerated/eager effort (by the investors or their advisors) to “protect” their investment.

4. How does a down round impact the company’s founders and employees?

Various stakeholders will perceive a down round differently.

For the existing shareholders - including early investors and founders - a down round can have varying dilutive effects on their shareholding interests as well as some demoralising impact. The dilutive effect is made worse if investors in the Reference Rounds (such as VCs) have secured anti-dilution rights to be issued additional top-up securities. Founders and pre-seed investors (such as family and friends) are unlikely to have had similar anti-dilution rights as ordinary shareholders. Mixed with the legal and shareholding implications, a down round can shatter the economic share, morals and drivers of the founding team members.

Employees face a similar situation to the founders. A down round can impact the company’s morale badly. This is made worse if employees have some economic interest in the company. They may have been issued employee share options with an exercise price at prior fair value of the company. The exercise price of those options could now be higher than the fair value of the company’s shares in a down round, which makes them “underwater” and not worth anything economically. Even if the employee share options are not underwater, the employees’ stake in the company would have reduced under a down round affecting their potential returns. While rare, some employees may have exercised their options into shares already, which in most cases are ordinary shares without anti-dilution rights. A down round (with anti-dilution rights) can demoralise such employees who have economic interest in the company, and so backed and worked to create value in the company. The board must consider the economic and emotional impact of a down round to the employees and appropriate remedial actions. Based on the underlying employee share scheme documentation, the board may have the power to adjust the exercise price of the options or issue new options to compensate the employees. In some instances, the board may consider a special issue of shares if it has the power to do so.

5. How does a down round impact the company’s investors?

For VCs and investors that have secured anti-dilution rights in the Reference Rounds, they will have a level of comfort that the down round will not be as detrimental to them as to the ordinary shareholders. These investors should be issued additional shares under the anti-dilution rights mechanisms, which dampens the negative economic impact on their shareholding. On the other hand, for some VCs and institutional investors, accepting a down round could also mean marking down the value of their investment. If the company takes up a big proportion of the investor’s relevant VC or investment fund, this could affect the potential carry/returns for the investor. These investors may also be concerned about the morals of the founders and employees, whose ordinary shareholding may be much more negatively affected by a down round. If these concerns are serious, investors with anti-dilution rights could agree to waive or limit the effect of the additional top up securities or push the company to avoid the down round as much as possible.

While we won’t get into the mechanics of different anti-dilution rights, it is interesting to note how this right works in New Zealand versus overseas. In New Zealand, the anti-dilution rights almost always result in additional shares (often preference shares) being issued at nil consideration. Overseas, the anti-dilution rights change the conversion price or ratio for which preference shares convert into ordinary shares in an exit event. It does not result in new shares being issued after the down round. The difference is that in New Zealand, the company and new investors participating in the down round need to be very clear on the pre-money and post-money capitalisation table (including because of the issue of the top up shares). It is also unclear whether in a liquidity event where a preference shareholder elects to be paid their liquidation preference, the investors who have been issued additional preference shares under anti-dilution mechanisms can claim to be paid a higher amount than their original investment. This would depend on the exact wording of the governing documents and the terms of the liquidation preference, but it would appear arguable that in New Zealand, the liquidation preference could increase more than the initial investment amount in this case.

Finally, there are investors participating in a down round. Investing at a lower valuation than previous rounds would present a good economic opportunity. However, there are concerns too. First, being involved in such rounds, especially as a lead investor (for VCs or institutional investors), can leave a bad taste in the market for their reputation as well as to the founders and earlier investors. This is made worse if the terms of investment are negotiated above and beyond what are typical (see above). Secondly, if the investor participating in a down round has a representative on the board of the company, there would inevitably be questions of conflict. How can you serve as a board member and approve terms of a down round to be in the best interests of all existing shareholders and the company, while also benefiting from it as an investor on the other side with all its adverse economic impact?

6. How should the board authorise a down round?

Given the scrutiny attached to down rounds, boards approving down rounds should follow corporate governance best practices for decision-making and any applicable contractual or statutory provisions. These include the rules under the company’s governing documents and the Companies Act 1993 (the Act). We focus on the legal aspects below.

First, the board of directors should carefully review and follow their governing documents. While the new investors may negotiate the terms of these governing documents further, a down round should be authorised according to their current or revised form. This may mean obtaining special board or shareholders’ approval for the share issue, following the pre-emptive rights process set out in the company’s governing documents (if section 45 of the Act is negated or modified by them) or, if there is a power to waive existing shareholders’ pre-emptive rights, considering the appropriateness of exercising that waiver power. These will be company-specific.

The board members should also be mindful of the statutory obligations that apply to them under the Act. Among other rules, under section 47 of the Act, before the board of a company issues shares without unanimous shareholder approval, it must resolve that in its opinion the consideration for and terms of the issue are fair and reasonable to the company and to all existing shareholders, sign a certificate to the same effect and delivering a copy of it to the NZ Companies Office. A board may genuinely believe that raising capital in a down round may well be critical to the ongoing viability of the company and so in the company’s best interest. But it may also be the case that the outcome of a down round results in one or more existing shareholders’ interests becoming so diluted and immaterial, that it would have been better not to have done a down round, perhaps opting instead to sell or liquidate the company, or looked for other ways for the company to operate. Failing to comply with section 47 is deemed to be conduct which is unfairly prejudicial to shareholders or former shareholders, and can result in statutory offences under the Act. There are also general directors’ duties that apply. A director must act in good faith and in what the director believes to be in the best interests of the company, exercise power for a proper purpose, and not act in a manner that contravenes the Act or the company’s constitution.

Another statutory issue is regarding the disclosure of directors’ interests. It is usual for companies to have an investor director who is appointed by an investor group. If the same investor or shareholder group is leading or participating in the down round, the investor director will need to ensure that their interests are fully and properly disclosed and recorded in the interests register of the company. These disclosures should also include the additional shares that may be issued at nil consideration under anti-dilution mechanisms. Under the Act, it is possible that the company may void the transaction in which a director is interested at any time before the expiration of 3 months after the transaction is disclosed to all the shareholders (whether by means of the company’s annual report or otherwise). This is unless the company has received fair value under the transaction. In turn, this will depend on the information known to the company and to the interested director at the time of the transaction, and whether it was entered into in the ordinary course of business and on usual terms and conditions.

7. Recommendations for the board

A down round is just another capital raise. The same rules that apply to companies when raising capital apply to down rounds. However, it has special considerations because of its negative context and implications for various stakeholders. As a potential guidance, we set out a few non-exhaustive recommendations for the boards navigating the tricky waters of a down round:

Consider the alternatives: Explore all other options before considering a down round. Some of these are easier said than done, but they should be explicitly set out in an options paper for board discussion:

Are there ways to extend the cash runway by increasing revenue and reducing costs? For SaaS companies, is it possible to offer pre-paid annual subscriptions that bring forward revenue with some discount? Are there meaningful cost-cutting opportunities – subscriptions, rent, contractors or other personnel – that can be implemented? Extending the cash runway even by a few months makes the company more attractive for investment with more leverage, and could delay the capital raise until there is a more opportune time to avoid a down round.

Are there alternative, non-dilutive financing options available? If the company is generating sizable revenue, it may be possible to obtain venture debt or other revenue financing capital. Could the company at least seek a flat round? If there’s any allocation remaining from the Reference Round, could these be filled up? Would existing investors support a minimum capital raise on a flat or a very slight up round to increase the company’s runaway? Could you do this with a convertible note or a SAFE that pushes out the valuation exercise?

If not a raise, could the company just exit? What is a realistic estimate of the sale price that can be achieved under the market condition and the funding needed to get to the completion of the sale?

Board makeup and negotiation: If the board has sufficient members, it should form a sub-committee of independent and disinterested directors (or at least a non-participating director) to negotiate and evaluate the down round. If possible, get a disinterested new investor - as opposed to an existing shareholder - to lead and price the round, and set other investment terms. If only existing investors especially those with anti-dilution rights are involved in the down round, objectivity and conflicts could be questioned more readily, in which case the board should emphasise fuller and prior disclosure of interest to the stakeholders. To support a claim that the deal was bargained in good faith at arms-length, the board should seek pro-company terms, such as lowering liquidation preferences (or ensuring it is no more than 1x), eliminating any participating preferred features, adding “pay-to-play” provisions (where if the preference shareholder does not participate in subsequent capital raising events, their shares convert into ordinary shares), watering down veto protections, increasing ESOP pool on a post-money basis, among other things.

Approval process: Obtain all approvals required under its governing documents and the Act, including resolving the fairness and reasonableness of the terms and conditions of issue to the company and all existing shareholders and declaration of actual or perceived conflicts. It may also be prudent to go above and beyond the statutory and contractual requirements and obtain:

written recommendation and approval from disinterested directors; and

written approval from at least a majority of the shareholders and a majority of the diluted shareholder classes – if the shareholding size is less than a dozen or so, then consider obtaining unanimous approval.

The board may obtain an independent third-party valuation to justify the down round valuation. However, this may be cost-prohibitive and perceived as self-serving.

Pre-emptive offer to the shareholders: Offer the existing shareholders to participate in the down round. While the pre-emptive offer does not immunise the board from their statutory duties, it demonstrates equal treatment of the shareholders and the chance to retain their pro rata shareholding in the company. The offer period is generally 2 weeks, more or less.

Communication to shareholders: Consider a proactive information update addressed to shareholders:

Explaining the options the company considered for raising capital and why a down round was determined to be appropriate.

Describing the anti-dilutive effects of issuing securities in a down round and disclosing the negative impacts to the existing shareholders.

Offering all existing shareholders the right to participate in the down round on a pre-emptive basis or, if not, why not.

Seeking a written shareholder approval of the down round.

Similarly, the board should proactively communicate with their employees about the down round. Finding out about the down round through work gossip or the media will likely have a negative narrative and affect team morale. Having an upfront communication can help the board control the narrative and provide comfort to the company staff. It can also be used to address how employees who are underwater on their share options will be treated going forward.

Records: Have good written records of the down round authorisation process, including the minutes from the final board meeting approving the raise. The board minutes should:

contain a record of the alternatives considered, market checks, outside financial advice (if any), approval of independent sub-committees, efforts to protect the diluted shareholders and employees, and other steps taken in the process of completing the financing;

demonstrate, genuinely, why the down round was necessary and how the terms and considerations for the issue of shares are fair and reasonable to the company and all existing shareholders; and

record all directors’ interests in sufficient detail.

What next

If you have any questions regarding this article, get in touch with Joshua Woo.

If you liked reading this content and want more, please subscribe here.

Disclaimer

This publication should not be construed as legal advice. It is necessarily brief and general in nature. Please seek professional advice before taking any action in relation to the matters discussed in this publication.