‘Pump-and-dump’ - Manipulation of Markets

The Australian Securities and Investments Commission (ASIC) has recently made the first social media related ‘pump-and-dump’ conviction, warning traders that the use of social media to coordinate ‘pump and dump’ schemes may amount to market manipulation. The trader (online name “Fibonarchery”) manipulated the share prices of 20 stocks, using 13 different trading accounts in the names of his friends and family. He aimed at moving the share prices of companies listed on the Australian share market by posting on social media, illegally disseminating information about his wash trades and dummy bids, seeking to increase the share price, then selling the listed stocks at a higher price. The trader is facing a maximum penalty for each charge of 10 years in prison, a fine of up to AUS$765,000, or both.

What is ‘pump-and-dump’?

A ‘pump and dump’ activity is a form of securities fraud where an individual first encourages others to buy a particular stock, for example by spreading false or misleading information on social media to increase (or ‘pump’) its market price. Then once the price and volume have increased as a result of artificially generated demand, the individual sells (or ‘dumps’) shares that the individual held since before the artificial price increase to make a profit from the price rise.

It is a classic case of market manipulation.

Although market manipulation has existed for as long as tradable assets have existed, the increasing use of online trading platforms and the largely unregulated cryptocurrency market is seeing greater occurrences of these ‘pump and dump’ schemes.

Is traditional ‘pump-and-dump’ scheme illegal?

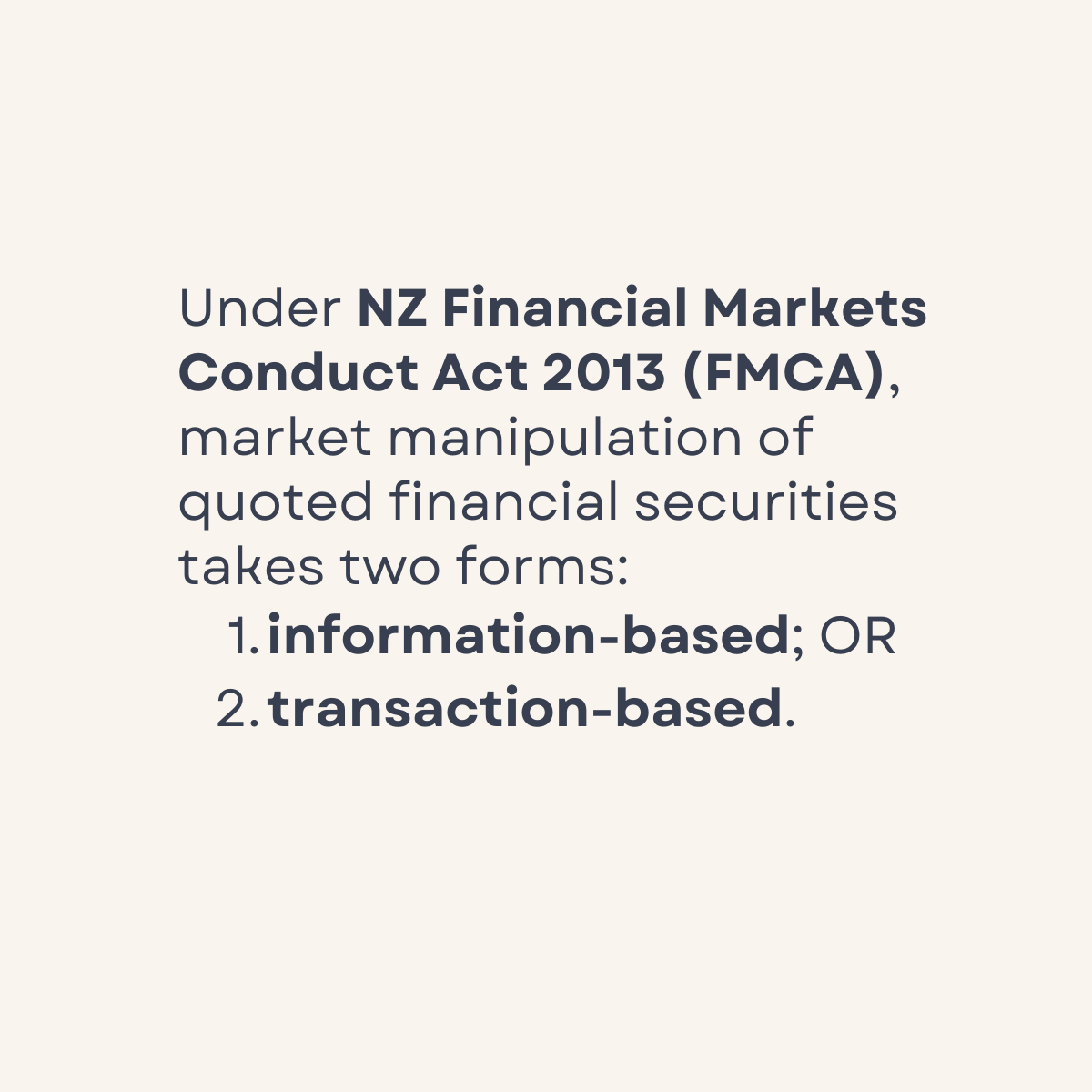

In New Zealand, ‘pump-and-dump’ schemes for financial products are considered market manipulation, which is prohibited under Part 5, Subpart 3 of the Financial Markets Conduct Act 2013 (FMCA).

The FMCA includes provisions for two types of market manipulation:

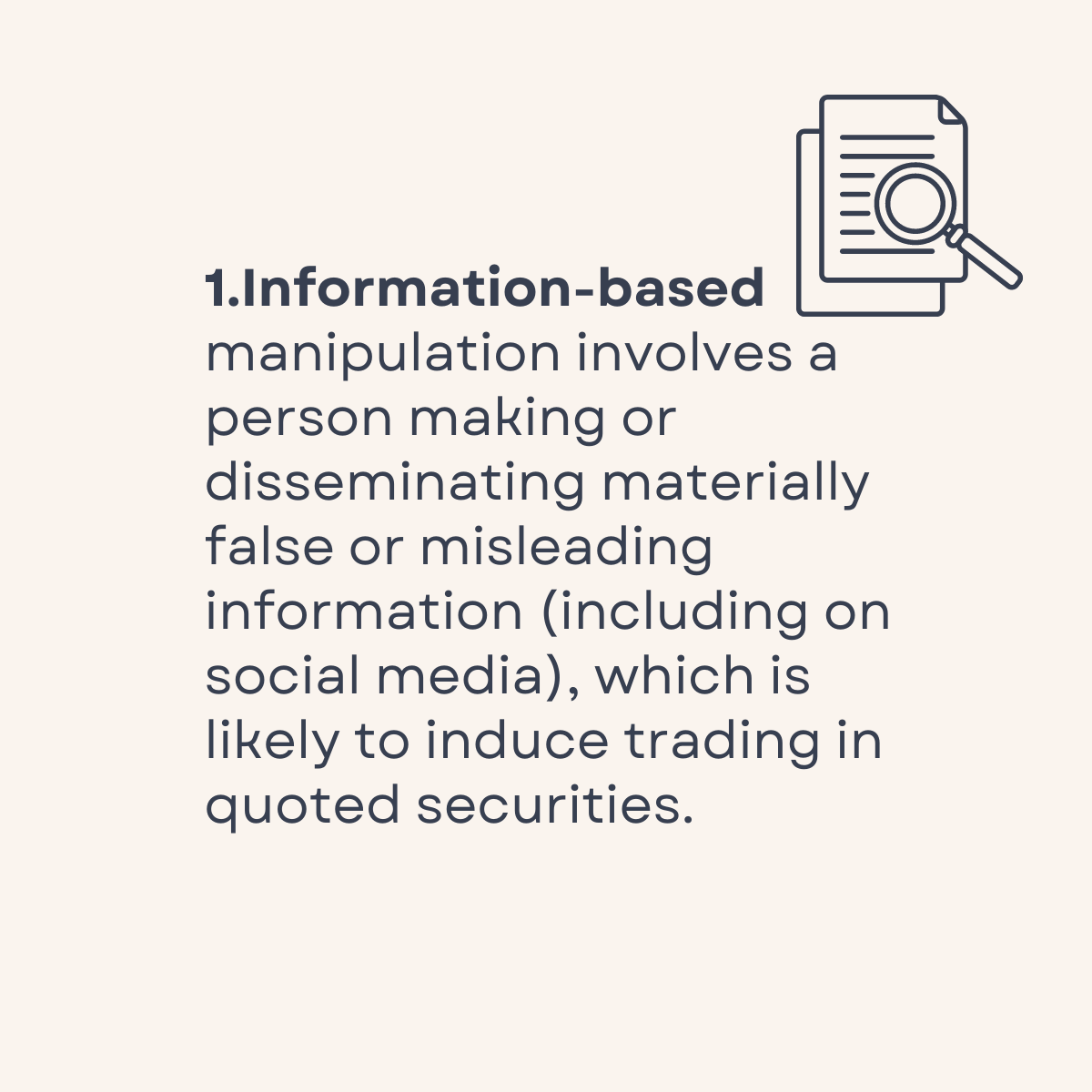

Information-based manipulation: Information-based manipulation relates to a person making or disseminating information about a financial product, that they know or “ought reasonably” to know contains information that is false or materially misleading. Market manipulation occurs if the information shared is likely to make a person trade in that product, or distort the market price valuation. A ‘pump-and-dump’ scheme is an example of information-based manipulation, where the manipulator shares information which is likely to make a person trade in a product or affect the price.

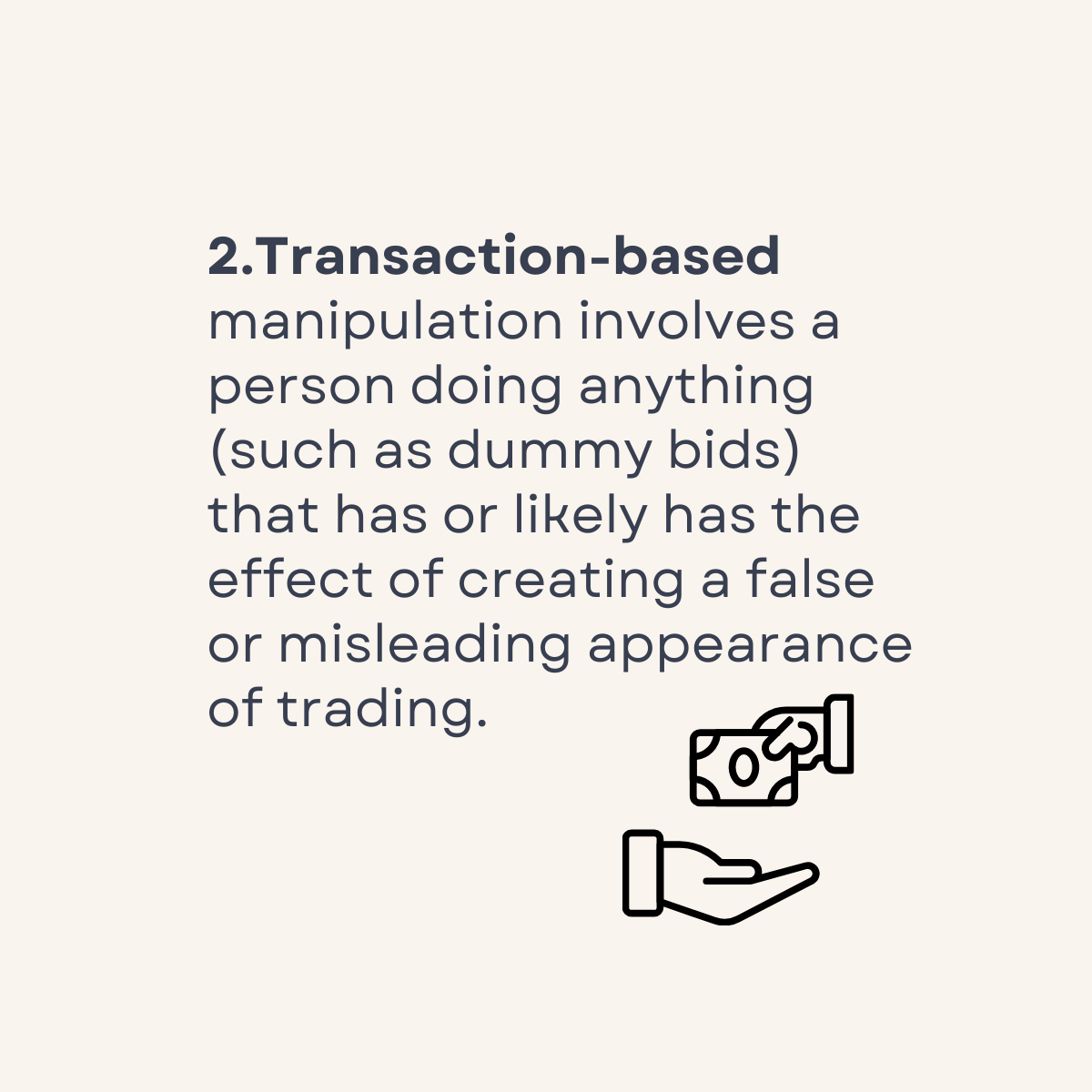

Transaction-based manipulation: Transaction-based manipulation relates to a person’s actions. This occurs when a person makes trades that may give market participants a false or misleading impression about a financial product. The person must have known or “ought reasonably” to have known such action would give a false or misleading impression.

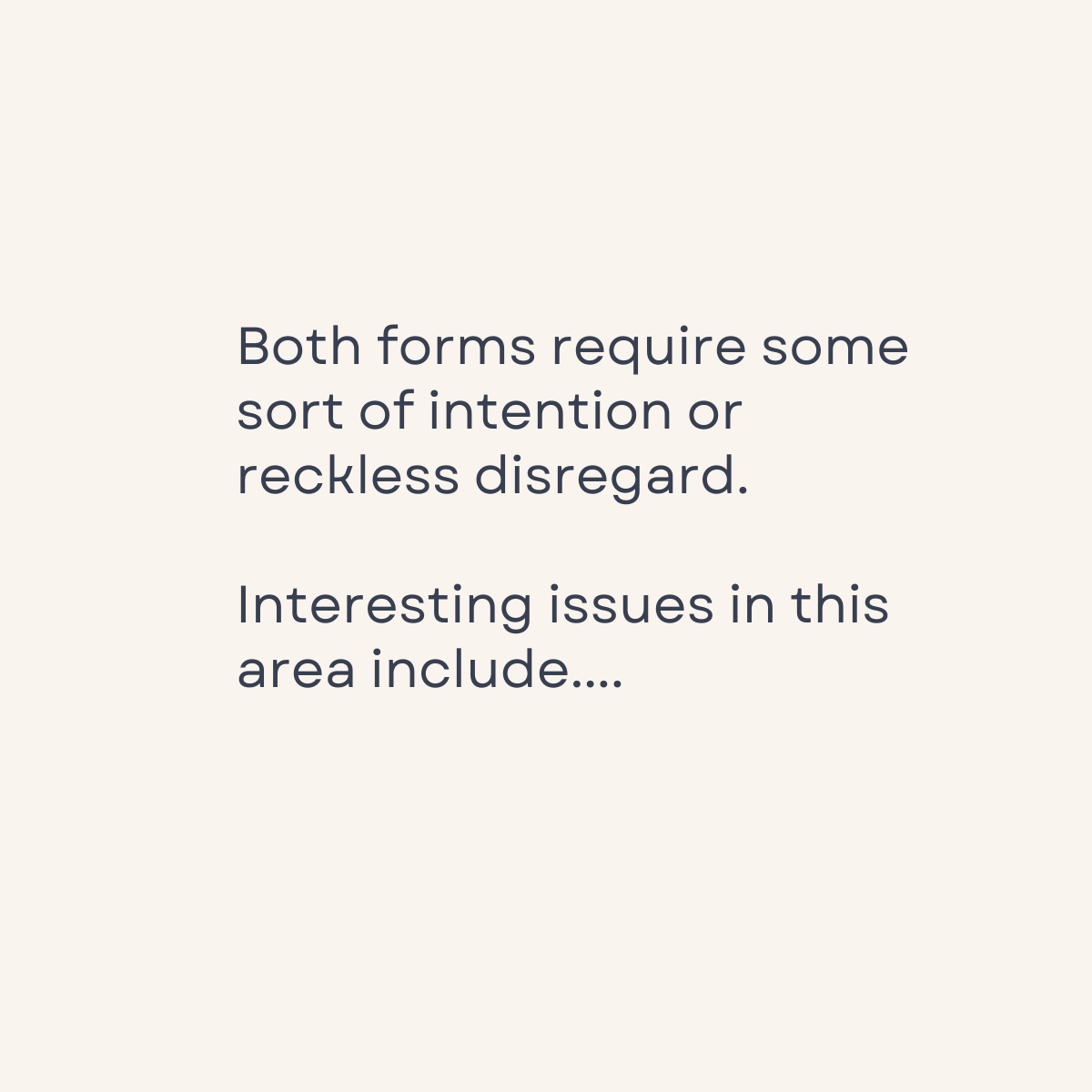

For both types of manipulation, it is not a defence for a person to claim they simply “did not know” that what they said or did would give a false or misleading impression. If the person’s distribution of information or action was “likely to” result in the circumstances explained above for each type of manipulation, the person may be in breach. The volume, value of an order, or the fact that there exists any financial gains are also irrelevant if its purpose was manipulation. (There are some exceptions to these provisions.)

In most serious cases, market manipulation may amount to a criminal offence and result in imprisonment of up to five years, and a maximum fine of $2.5 million for a company or $500,000 for an individual.

Regulating market manipulations such as ‘pump-and-dump’ schemes is important as it may have an impact on investors’ confidence, limiting participants’ informed participation in financial markets. Any reduced demand for investment would ultimately hurt the economy by making it harder for New Zealand companies to compete and raise capital investment in their business.

Cryptocurrency market

In the eyes of the FMA (and arguably, the law), cryptocurrencies are not legal tender (in other words, money that must be accepted as payment) nor financial products. So, the FMCA provisions relating to market manipulation do not apply to cryptocurrencies and there are no crypto-specific rules regulating the crypto market in New Zealand.

Investors should be more cautious in the crypto market as there have been blatant attempts by bad actors, spreading fake recommendations to promote ‘pump-and-dump’ schemes. In a similar fashion as with stock, having previously bought up a coin in large amounts, the bad actors can sell their holdings of the coin at the peak for a profit. For example, there was a case where a fake Twitter account purporting to belong to the founder of a cybersecurity firm tweeted support for a new digital coin. As a result of this post, the price of the coin jumped in four minutes and trading volume doubled. Not long after, the price went back down, after the participants of the scheme had ‘dumped’ their holdings. This whole campaign was organised by a key player in a ‘pump and dump’ scheme that was organised by users of an online chat room.

There is an ongoing debate on whether the crypto ecosystem will manage to function efficiently with no clear rules to control such market manipulation activities. It is likely that cryptocurrencies will face more regulation going forward and New Zealand may soon have to adopt restrictions and increased control in the crypto market to stay in line with other countries.

Other recent updates

Archegos case

In the US, the Securities and Exchange Commission (SEC) initiated a case against the founder of Archegos Capital Management for artificially and dramatically driving up the share prices of a few tech companies by purchasing billions of dollars of total return swaps on margin. SEC claims that the founder has used his firm to orchestrate a market manipulation scheme that caused a huge shockwave across the US securities markets. The counterview is that Archegos engaged in a bullish buying activity in a bull market for tech stocks. Purchases alone probably would not necessarily constitute an illicit market manipulation activity. So, it will be an interesting case to see whether the prosecutors can prove the manipulation charge by convincing a jury beyond reasonable doubt that the founder intended to artificially inflate stock prices beyond ordinary supply and demand.

Use of online platforms

With the growth of ‘DIY’ investing on online trading platforms such as Sharesies and Hatch, social media pages where investors share their investment information have proliferated. Many users find these pages a useful source of information for making investment decisions. But, there is also a concerning trend of social media posts being used to boost a stock's price based on false, misleading statements, which can amount to market manipulation.

Last year, the FMA filed proceedings against the CEO of a listed company for the anonymous posts he made about the company on an online investor forum, which the FMA considered to be false and misleading representations. Following this case, the FMA warned investors to be careful using online platforms as their source of investment information as they can be “exploited by vested interests”. The FMA again raised similar concerns in its 2021 Annual Report, noting the regulator had issued a warning to an individual for actions that took place on an online trading platform and likely amounted to market manipulation. The FMA considered this as an opportunity to highlight and remind investors of their obligations and responsibilities regarding trading activity via online platforms.

What next

If you have any questions regarding this article, get in touch with Joshua Woo.

If you liked reading this content and want more, please subscribe here.

Disclaimer

This publication should not be construed as legal advice. It is necessarily brief and general in nature. Please seek professional advice before taking any action in relation to the matters discussed in this publication.