Shareholders’ agreement: FAQs (UPDATED)

A shareholders’ agreement is a confidential agreement between the shareholders of a company, governing:

the relationship between the shareholders;

their relationship with the company; and

key matters like exits, governance and decision making, raising new capital and dispute resolution.

In the startup world, it is also called a (co-)founder agreement, but they serve the same core function. There is no legal requirement to put in place a shareholders’ agreement, but in most cases it will be a good idea to have one.

Below, we answer some commonly asked questions about shareholders’ agreements:

1. Should you have a shareholders’ agreement?

2. What key items should be included?

3. What protections do financial investors expect?

4. Is it different from a (co-)founder agreement? What’s founder vesting?

5. How do you future proof it?

6. Do you need a constitution as well as a shareholders’ agreement?

7. What are some common mistakes to avoid when drafting a shareholder's agreement?

1. Should you have a shareholders’ agreement?

Yes, because not having a shareholders’ agreement can create awkward and unsatisfactory outcomes especially when things go wrong. If you do not have a shareholders’ agreement (and there is no legal requirement to have one), the default rules under the Companies Act 1993 will apply. The default rules are designed to capture the lowest common denominators in most company environments. This can be problematic because either the default positions under the Companies Act are not appropriate for the shareholders or the company in question, or the Act is silent on particular governance matters.

For example, some common potential issues under the default legal rules are:

Fully vested shares: Where shareholders are co-founders, there’s no default rule to deal with those who disengage or want to exit. So a co-founder who is no longer interested in contributing to the growth of the company will remain an equal shareholder. It gets very difficult to navigate the future of the company (including raising capital or motivating the remaining founders).

Board control by simple majority: Directors must be appointed by “ordinary resolution” – a simple majority of the voting shareholders. The directors form the board, and the board oversees and is responsible for the management of the company. So whoever has a simple majority of the shares control the company. If you hold less than 50% of the shares, you have no say on director appointments and even if you are a director initially, you can be removed by those who hold a simple majority.

Unrestricted share transfer: Shares are freely transferable to another person. If your co-founder decides to sell their shares to a competitor, your competitor becomes your new partner.

No built-in dispute resolution: If there is a dispute between the shareholders, the Companies Act does not specify how you can resolve them. Your options are commercial negotiations if everyone is willing, being stuck in the status quo, or costly litigation.

No IP or non-compete protection: Shareholders can freely compete with the company while they are a shareholder or after they leave the company. Complicating this issue further, it will not be clear who owns the IP used by the company.

Limited veto rights for minority shareholders: If you have less than 25% of the shares in the company, you do not have a say on the more fundamental company decisions. These include decisions to sell the business and its assets, or to enter into key supplier or customer contracts that count as a “major transaction”, or to wind up the company.

In general – and especially if you are an equal co-founder or a minority investor – you shouldn’t be happy with the default rules. A shareholders’ agreement helps to make the rules more appropriate and fairer for the shareholders.

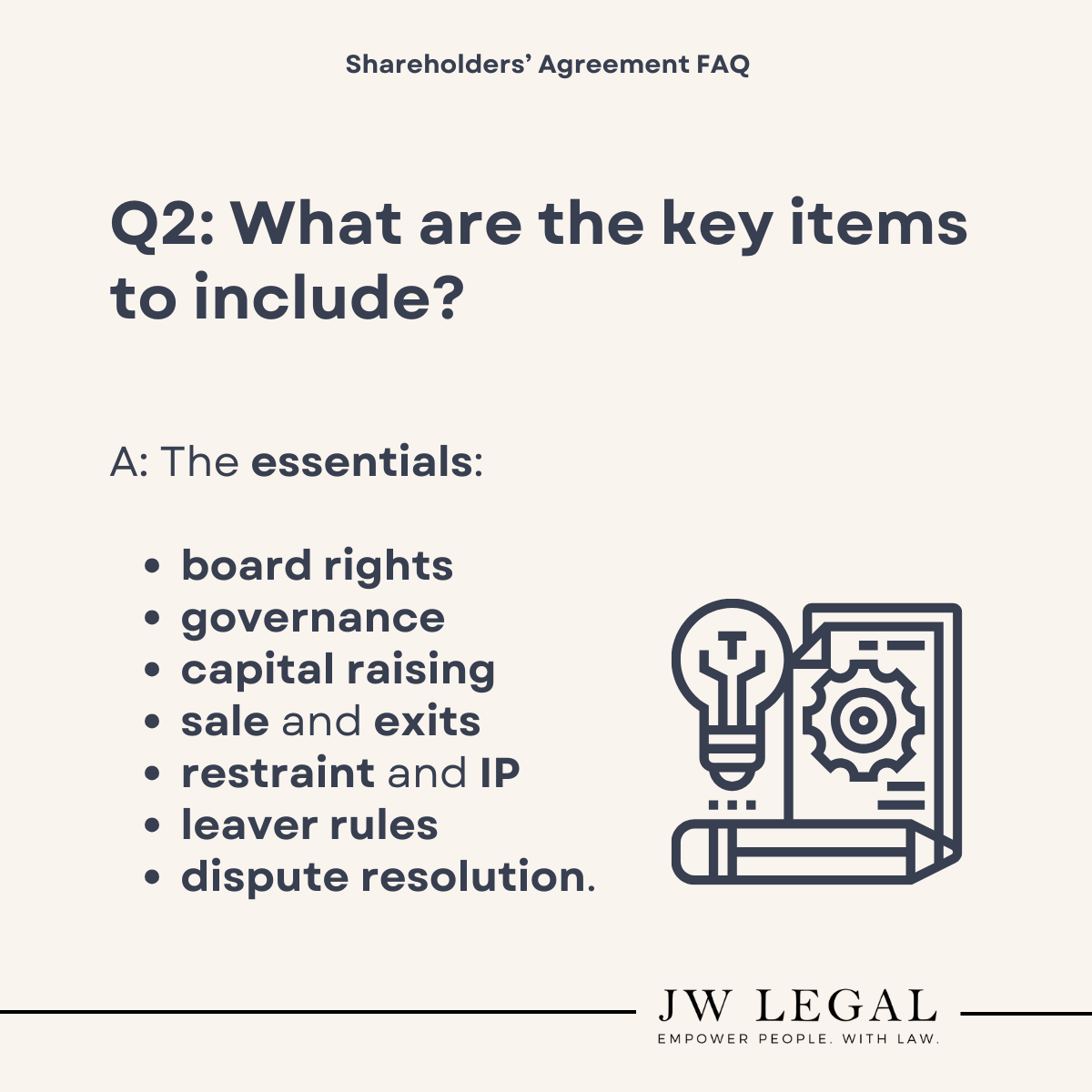

2. What key items should be included in a shareholders’ agreement?

The purpose of a shareholders’ agreement is to change the default rules or to add to them. There are no set rules. However, there are some key items that are frequently included:

Director appointment rights – Parties can agree that each shareholder can appoint a director even if each of them have less than a simple majority of the shares. The right to appoint a director may be “personal” (tied to the shareholders’ identity) regardless of their shareholding percentage or by number or by class (e.g. preference shares). In some cases, the right to appoint a director should be lost when your shareholding falls below a certain threshold.

Decision-making – The default rule is that the board makes decisions of the company, acting with a majority. The proviso is that in specific situations they may require shareholder approvals, such as when entering into major transactions. If you do not have a board seat or are in the minority as a board member or a shareholder, you may expect to have further say in that decision. It is possible to carve out specific corporate actions, such as entering into transactions over an agreed monetary threshold, to require a special board or shareholder approval (e.g. a 75% vote).

Governance and information – The shareholders’ agreement should include key governance items such as the frequency of the board meeting, the type of information the company should prepare for the board and their frequency, whether an initial business plan should be prepared and the frequency of its review (generally annual), and a dividend policy.

Capital raising – The company should have a broad outline of how it will go about raising new capital. If new shares are to be issued to raise capital, existing shareholders should have the first right of refusal to subscribe for further shares. Standard exceptions to this rule include issuing capital under an approved employee share incentive plan and, for more widely held companies, raising capital with dilutive effect that is less than, say 10-20% of the company over a 12-month period. If one or more shareholders are to lend money to the company, the shareholders may want to agree on how those amounts should be repaid and whether the company will grant the lender a security interest over its assets.

Sale and exit – If a shareholder wants to exit the company, the remaining shareholders should have a first right of refusal to purchase that shareholder’s shares. They may also wish to retain a right to veto any proposed third-party buyer on reasonable grounds, such as if the buyer is a competitor. Additionally, shareholders may want to include provisions that allow them to:

- Drag along all other shareholders in an exit event (e.g. sale of the company), or

- Tag along in a sale initiated by other shareholders.

Restraint and IP – Every shareholder has an aligned interest to protect the goodwill of the company. Non-compete and non-solicitation obligations help protect the business goodwill. Similarly, and especially for SaaS co-founders, they will want to make sure that the IP developed prior to and during their venture together vests in the company.

Founder vesting, good leaver / bad leaver provisions – These clauses set out different outcomes depending on how a shareholder exits (e.g. voluntary resignation vs misconduct), and determine the treatment of unvested or repurchasable shares.

Dispute resolution – A dispute resolution mechanism should help parties navigate their disputes and deadlocks, encourage voluntary settlements and avoid litigious processes and outcomes. Depending on the subject matter of the disputes, parties may want to include an expert determination process for a speedier resolution.

This is not an exhaustive list - every company is different, so the agreement should be tailored to its structure and priorities.

3. What protections do financial investors expect?

Where professional or strategic investors are involved, shareholders’ agreements often include provisions designed to protect their capital and influence:

Anti-dilution rights – Adjust investor shareholding if future shares are issued at a lower valuation

Information rights – Access to financial reports, management accounts, or board observer rights

Consent matters – investors may require veto rights on major actions (e.g. cap raises, asset sales)

Exit rights – Drag-along rights or put options if an exit event is not achieved by a certain time.

These rights are often non-negotiable for institutional investors and should be carefully balanced with founder autonomy. Separately, these investors could also insist on a separate class of shares that give them higher ranking liquidation or dividend rights.

4. Is a shareholders’ agreement different to a co-founder agreement? What’s founder vesting?

They broadly deal with similar shareholding terms in a company. How should co-founders – that is, initial shareholders – deal with each other and their shares? So the name of the agreement is interchangeable especially with the start-up companies.

Co-founder agreements also often include “founder vesting” terms. Founder vesting works by giving the company the option to buy back a co-founder’s initial shareholding if they cease to be a shareholder or work for the company, or they default in making an agreed contribution to the company. The number of shares that can be called under option will generally decrease over time and may or may not require a fair value to be paid for those shares. Founder vesting terms can also be a negotiation point for professional or financial investors.

A related concept is reverse vesting. While traditional vesting involves gradually granting shares to a founder over time, reverse vesting assumes the founder initially holds all their shares upfront but becomes subject to a buy-back right if they leave early. Over time, this buy-back right lapses in tranches, so the longer the founder stays and contributes, the more of their shares become fully secured. Reverse vesting terms can also provide for acceleration, meaning that some or all of the restrictions fall away immediately if certain events occur, such as a company sale or a founder’s termination without cause. This approach is particularly common in start-ups to align long-term commitment while still recognising the founder’s initial ownership.

Co-founder agreements also often reflect uneven initial contributions and expectations (capital, IP, time). These terms can be incorporated into a shareholders’ agreement to avoid duplication.

5. How do you future proof a shareholders’ agreement?

This can be a difficult, undesirable task when initially preparing a shareholders’ agreement. It is not practical to contemplate and set out every eventuality that may surface with a company. Rather, the goal should be to make sure that the shareholders’ agreement will be binding on all shareholders – present and future – and has flexible and fair mechanisms to change in the future.

Once a shareholders’ agreement is signed, it will be binding on the initial shareholders. Typically, it will be a term of the shareholders’ agreement that no other person can become a shareholder of the company (by being issued new shares or being transferred existing shares) unless they agree to be bound by the terms of the shareholders’ agreement. This ensures that the shareholders’ agreement continues to be binding on current and future shareholders.

As the company grows and the shareholders increase or decrease in size, the initial terms contemplated by a shareholders’ agreement may no longer be appropriate. In these cases where change is inevitable, every party to a shareholders’ agreement must agree to amend the agreement to reflect the new circumstances of the company. A unanimous agreement may be difficult or impossible to achieve if there are shareholders who will be disadvantaged by the changes. One way a lot of the shareholders’ agreements deal with this situation is by having a 75% approval threshold to make changes to the agreement, except in limited situations. This rule is generally accepted as it is similar to the default position at law for adopting or changing a company’s constitution (see more below on why you need a constitution). The threshold can be lower or higher than 75% and helps the company to adapt to changing circumstances more practically.

6. Do you need a constitution as well as a shareholders’ agreement?

Yes. A constitution is a must and sits alongside the shareholders’ agreement. By law, a company may only take certain corporate actions if its constitution expressly allows them. For example, without a constitution expressly permitting it:

The company cannot buy back its own shares or hold them as treasury stock.

The company cannot put in place a directors & officers liability insurance or provide an indemnity in favour of its directors or officers.

The directors must always act in the best interest of the company – and not in the best interests of a holding company or their appointing shareholders even in joint venture settings.

While a shareholders’ agreement is a private and confidential agreement between the shareholders of the company, a constitution is a public document. It must be filed with the Companies Office and is viewable by anyone on the public register. It may not be desirable to share the sensitive details of how a company is run (such as how its financial information is shared and its dividend policy). So these matters are recorded in the shareholders’ agreement, while the constitution is adopted and registered to ensure that the company has the flexibility to take the desired corporate actions.

The two documents work together: the constitution allows the company to do certain things, and the shareholders’ agreement governs how and when those things are done.

The current government is proposing a series of Companies Act reforms, which could take away the need for a constitution in the first place. We’ll keep our audience updated.

7. What are some common mistakes to avoid when drafting a shareholders’ agreement?

Even well-intentioned agreements can fall short in practice. Some common pitfalls include:

Using off-the-shelf templates that don’t reflect the specific shareholding structure or business model;

Not updating the agreement as new shareholders join or the business pivots;

Reliance on “handshake” or verbal agreements between founders without formal documentation;

Failing to enforce deed of accession requirements for incoming shareholders; and

Conflicting terms between company’s constitution and the shareholders’ agreement.

For more info & upcoming event

If there are any other questions regarding shareholders’ agreements, please feel free to reach out to Josh Woo, or let us know (we may add them to this FAQ page).

If you liked reading this content and want more, please subscribe here.

Disclaimer

This publication should not be construed as legal advice. It is necessarily brief and general in nature. Please seek professional advice before taking any action in relation to the matters discussed in this publication.