Convertible Notes Part 1: The Why and What

There are arguably hundreds of ways for a company to raise money. A predominantly popular method is convertible notes. A convertible note is a loan by an investor to a company, which converts into equity when a predetermined trigger event occurs. It is an easy way to raise money, will take up less time and (professional) money to put in place, and is robust enough to be used for early-stage companies as well as more mature companies looking to get listed as part of their pre-listing round.

In this two-part series, we cover:

Why and what – The key uses for convertible notes and why they are used. We’ll also look at four key features of convertible notes, including what we see are their standard market terms.

The alternatives – SAFEs (“simple agreement for future equity”), which are more founder-friendly, and priced equity rounds, which involve valuation exercises and negotiations over shareholding terms. We finish off with other considerations when issuing convertible notes, and perhaps why talking to a lawyer might make sense.

Why do we use convertible notes?

Convertible notes are used widely by early-stage growth companies that have not yet carried out a priced equity round. The startup community calls this a pre-seed or a seed round, typically targeting family & friends of the founders, some family offices, angels and venture capitalists. The pre-seed to seed round aims to raise between $100,000 to $2 million, which helps the company to accelerate its growth by hiring more talent to develop the product.

Convertible notes are also used by more mature companies. The key example here is companies preparing for listing on a stock exchange. In Australia, companies that are looking to get listed on the ASX are more frequently raising bridge capital via convertible notes. These companies raise larger amounts of up to $125 million, reportedly in the case of Till Payments. It wouldn’t be surprising if we see more mature NZ companies raise bridge capital before their IPO (or direct listings, for that matter) in the same way in the next few years.

So why do we use convertible notes? Here are the key reasons:

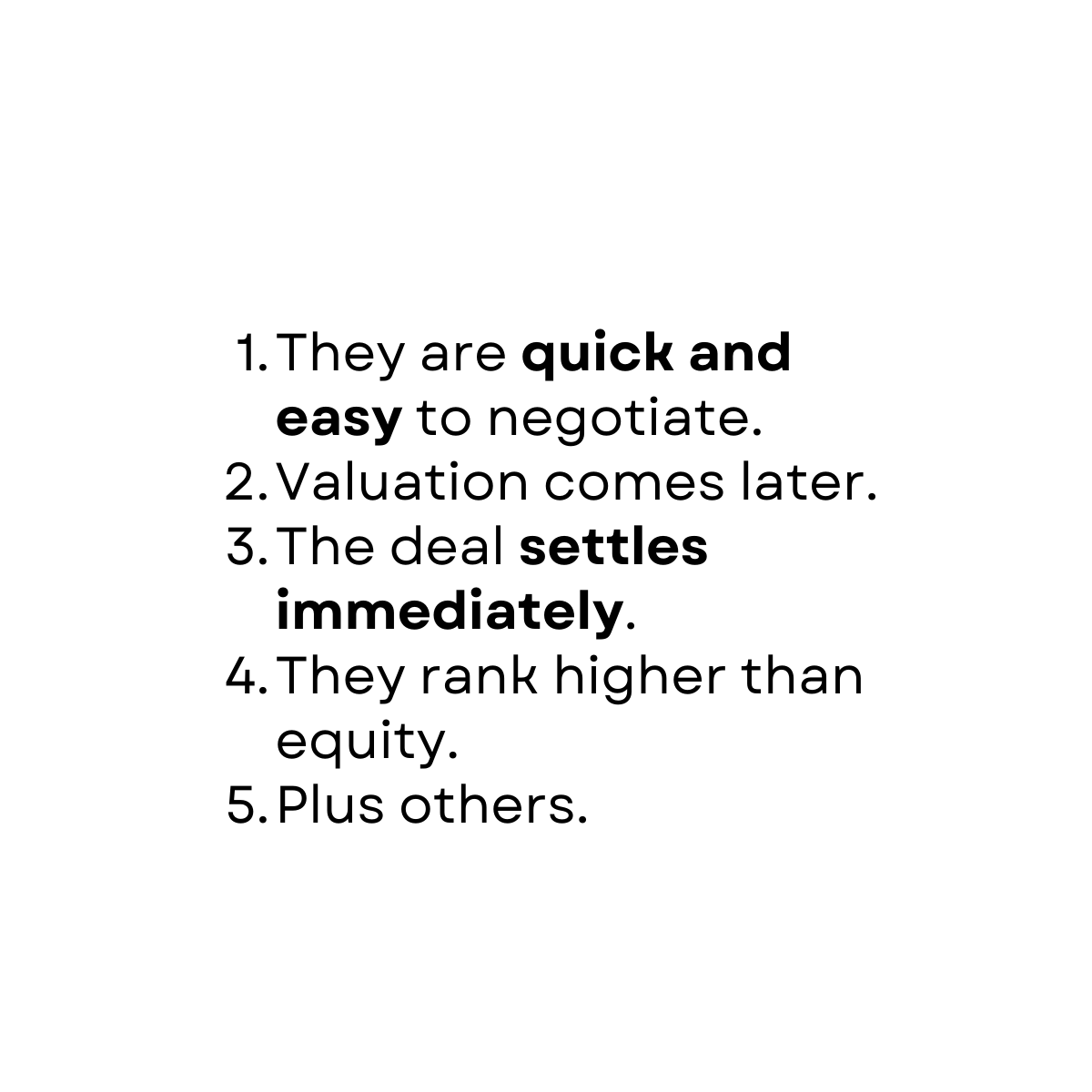

They are quick and easy to negotiate. Negotiating a convertible note is a relatively easy exercise compared to negotiating a priced equity round. Parties focus on the four key features discussed below and they can reach a deal quickly. Professional advisors play a smaller role too, so the legal and other professional costs should be significantly lower than if you were carrying out a priced equity round.

Valuation comes later (but cannot be avoided). More importantly, parties are deferring the valuation exercise. Valuations are hotly debated and negotiated, and can take up significant founder/management time and effort. A valuation exercise also incurs more professional costs from both sides, including for carrying out due diligence to defend or verify the valuation. For early-stage companies carrying out a pre-seed round, they may not have enough data to support any valuation. So convertible notes are a good compromise between the company and the investors to put some money into the company, while deferring the valuation exercise. (However, valuation needs to take place at some point, including with costs associated with that. This is why pre-seed/seed rounds are also called “bridge” financing to a priced equity round.)

The deal completes immediately. The loan is advanced as soon as the convertible note is signed. Companies do not wait for other co-investors to commit to the investment round and do not need to satisfy pre-conditions more common in a priced equity round.

For pre-listing companies, there are also other benefits. Pre-listing companies have other benefits too. They may want additional cash runway for product or market development or get a reputable investor(s) on their books to bolster the upcoming roadshows and marketing for their listing. They may also like to remain private for as long as reasonably possible and avoid the compliance costs and disclosure obligations of a listed entity.

Convertible notes are higher ranking than equity. For investors, a convertible note has the added benefit that it is a debt instrument. So in case of insolvency, the noteholder will have a prior claim to the assets of the company than the shareholders.

Let’s talk about their key features

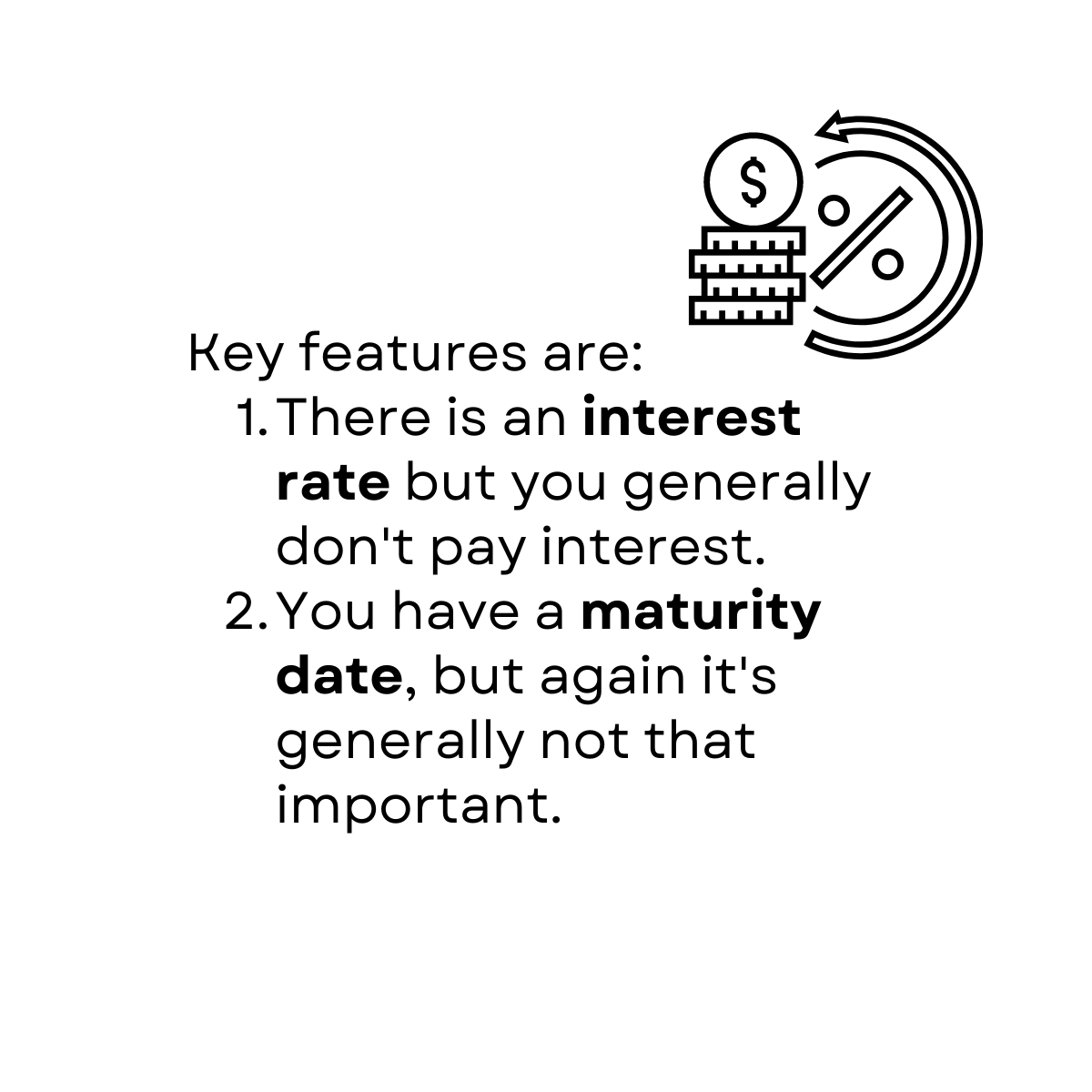

A convertible note is a loan agreement with added features. Four key features are:

Interest applies but you generally don’t pay it. A convertible note will have an applicable annual interest rate. In New Zealand, the rate typically sits at around 5% per annum. The interest is not paid out periodically. It instead accrues on the loan and is added to the principal loan amount (minus the applicable withholding tax) when the loan converts into equity at the conversion trigger event. Technically, the interest may also be repaid on the maturity date, although this is rare.

You have a maturity date, but this is generally insignificant. The loan will also have a maturity date. The market term appears to be 2 years from signing. After this date, the investor can demand repayment of the loan with accrued interest. A short maturity date encourages the company to carry out a priced equity round to trigger a conversion event. If there isn’t a trigger event by the maturity date, the company will remain at the mercy of the investor who can demand repayment of the loan and potentially put the company under. However, this rarely happens. Instead, the maturity date is generally extended or the repayment rights are waived or simply not exercised. To protect their investment, the noteholders will have an aligned incentive to allow the company to keep running and perhaps help them raise further capital. In most cases, this is the better alternative to potentially putting the company under and jeopardising their investment (and those of every other noteholder).

Priced equity rounds will trigger the conversion of the loan into shares. Convertible notes must define the qualifying events that trigger conversion. The main event is a priced equity round. A priced equity round is when the company agrees on its full valuation, negotiates terms of shareholding with the new round of investors and issue new shares to them. This is called a Series A round (and B and C and so on) in the startup community. When a priced equity round occurs, outstanding convertible loans will automatically convert at the same or discounted price, such as by applying a valuation cap or a discount rate, discussed below. Other conversion events include a majority share sale or major asset sale transactions, or a public listing event of the company.

Valuation cap and discount rates protect early convertible note investors. Convertible notes can include a valuation cap and a discount rate. A valuation cap is the maximum valuation that applies to convert the loan which applies even if the company is valued at a higher amount in the actual qualifying event. A discount rate is a discount of typically around 20% to the price per share paid by investors in the later priced equity round. Both the discount rate and the valuation cap are a function of rewarding noteholders for investing early in the companies, and recognising that company valuation that applies to them should be lower than the investors coming on board at a later stage.

Valuation cap/discount rate (an overly-simplified) example: Company X has a million outstanding shares with a $10,000 convertible note. It is about to complete a fully priced equity round at a $1 million valuation. If the note does not have a valuation cap, then the noteholder will be issued 10,000 shares at $1 per share ($1m divided by a million outstanding shares = $1 per share price). But:

Valuation cap of $500,000: if the note has a valuation cap of $500,000, the noteholder’s $10,000 loan will convert into 20,000 shares at $0.50 per share ($500,000 divided by a million outstanding shares = $0.50 per share price); or

A discount rate of 20%: if the note has a 20% discount rate, the noteholder’s $10,000 loan will convert into 12,500 shares at $0.80 per share, after a 20% discount to the $1 per share price.

There are other features too. Depending on which side of the fence you are sitting on, you may want to cover items such as conditions, an MFN obligation, pre-emptive rights and transferability parameters. A convertible note is essentially a contract and so all its terms are negotiable. While they can be relatively simple to negotiate, you should take care to make sure your position – as a company or an investor – is properly and fairly reflected in the agreement.

In the next part, we will take a look at the main alternatives to convertible notes and finish off with other key considerations when dealing with convertible instruments such as a convertible note.

What next

If you have any questions about how you can use or negotiate a convertible note, please contact Josh Woo.

If you liked reading this content and want more, please subscribe here.

Disclaimer

This publication should not be construed as legal advice. It is necessarily brief and general in nature. Please seek professional advice before taking any action in relation to the matters discussed in this publication.